June 10, 2026/

secfsn_plus is a canonical financial feature engineering layer built on top of SEC fundamental data. The project takes a wide...

Most financial analysis stops at ratios — revenue growth, margins, ROE. Those are useful, but they don’t tell you how reliable or persistent a company’s performance actually is.

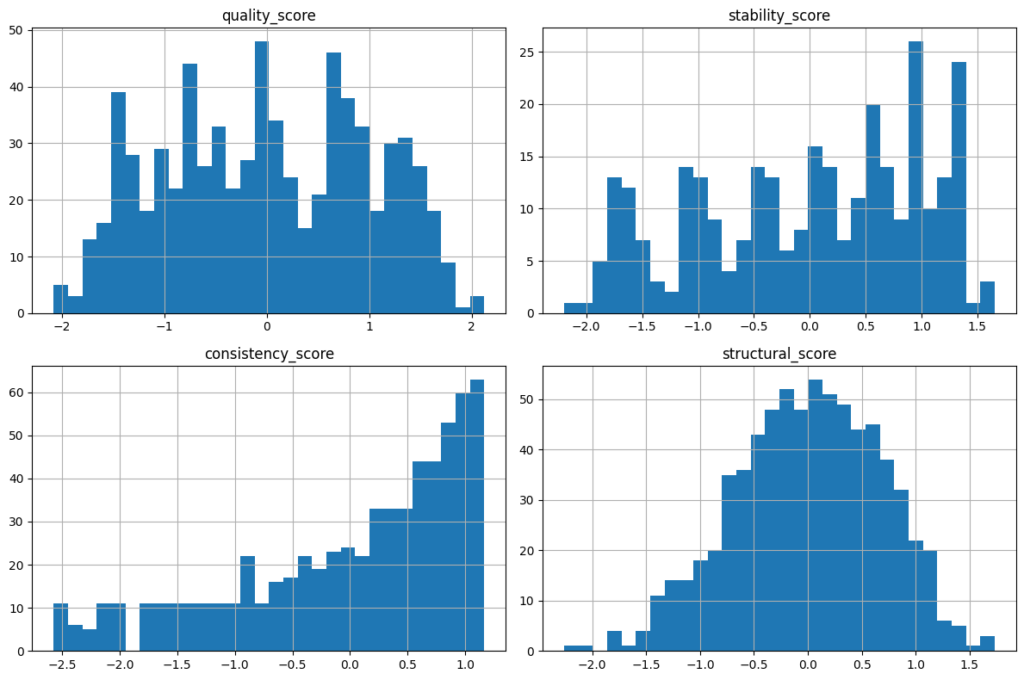

I built a structural feature layer on top of SEC financial data to focus on three things: earnings quality, stability, and consistency over time. Instead of just asking “what are the numbers today?”, the goal is to understand how those numbers behave across periods — whether they’re cash-backed, volatile, or structurally coherent.

At a high level, the system takes cleaned fundamentals and transforms them into a panel of structural signals, along with a composite structural_score that enables cross-sectional comparison between companies.

This project is part of a broader financial data pipeline:

Each layer builds on the previous one, moving from raw data → standardized features → interpretable structural insights.

Two companies can look identical on a snapshot basis but behave very differently over time. This framework helps surface that difference in a systematic and scalable way.

The output is a (company, period) panel of structural features + a scoring layer that can plug into screening, research workflows, or downstream models.

GitHub: Link