June 10, 2026/

Most financial analysis stops at ratios — revenue growth, margins, ROE. Those are useful, but they don’t tell you how...

secfsn_plus is a canonical financial feature engineering layer built on top of SEC fundamental data.

The project takes a wide SEC financial panel indexed by company and period, then transforms it into research-ready outputs: accounting ratios, factor scores, composite signals, screening outputs, and ML-ready feature matrices.

The important design choice is separation. secfsn handles the base SEC data layer. secfsn_plus handles deterministic feature engineering. Future layers can handle structural diagnostics, model training, or portfolio workflows.

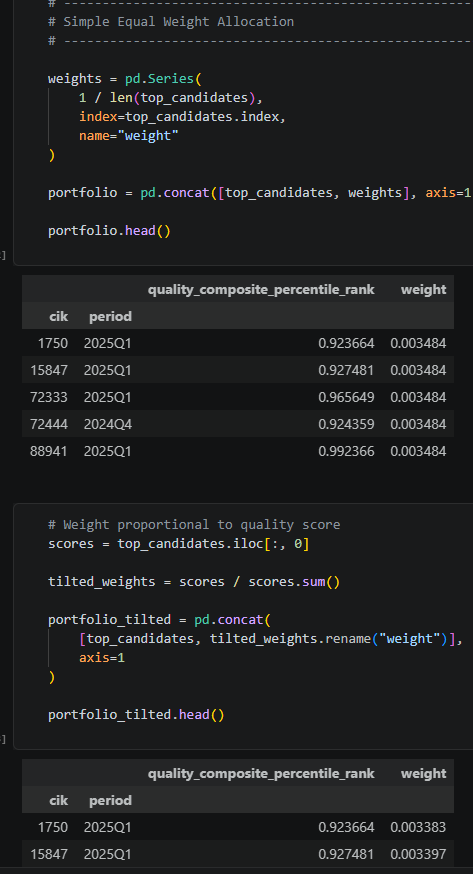

In the demo, I walk through the notebook workflow: starting with raw SEC/XBRL fundamentals, deriving standardized ratios, building factors and screens, then focusing on the final bridge into ML-ready datasets and trading-framework integration.

The goal is not to make investment recommendations. The goal is to create a stable, reusable feature layer that downstream research systems can build on.

GitHub link: https://github.com/rossautomatedsolutions/secfsn_plus